March 6, 2020

Financial Services

The Essentials of Debit and Credit Card Processing Fees!

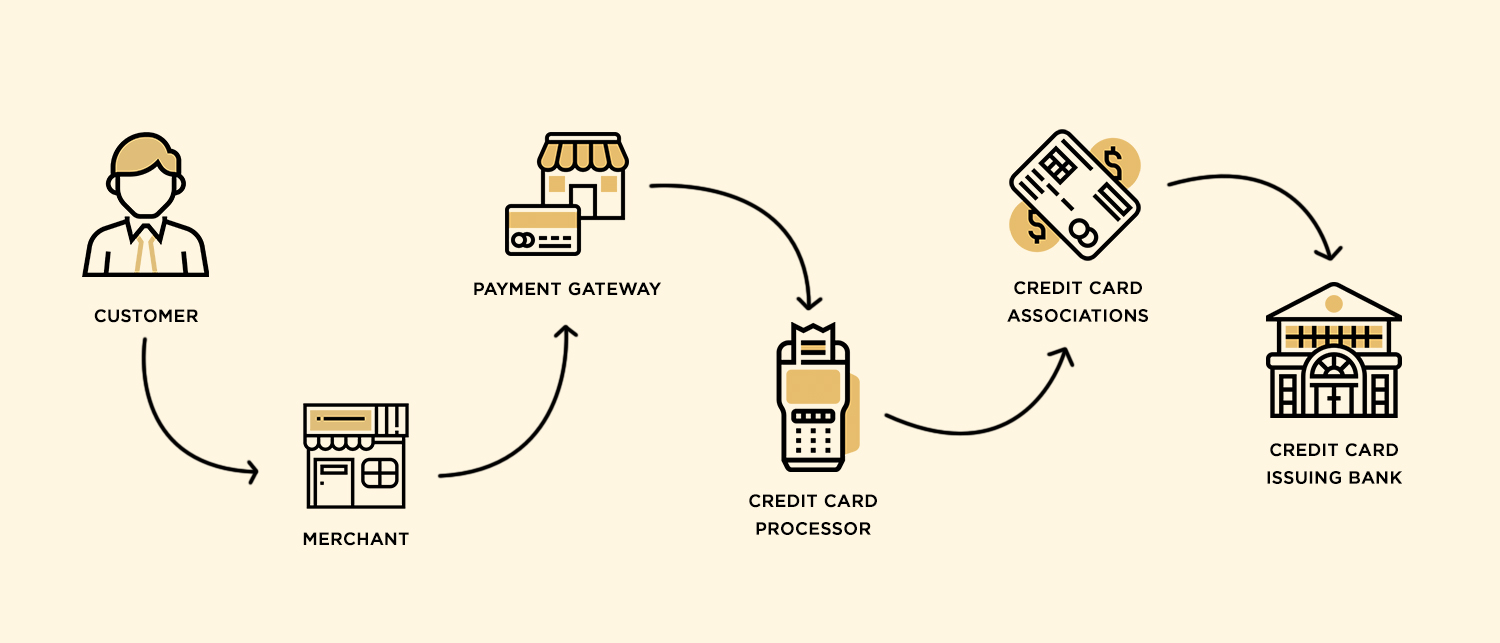

We live in the digital era. We live, eat and breathe digital. Everyday hundreds of millions of users buying stuff online and in retail shops, swipe, dip or tap their credit cards at stores or simply key-in their details online at payment checkout pages after selecting their purchases. Card transactions are indispensable for any business, whether it is online or offline. In short, card payments rule the markets now. Every card payment on the outside looks like a simple act of swiping your card at a terminal, but much more goes on behind the curtains as you enter your pin and ‘okay’ a transaction. Find out all about credit card processing fees and rates of the credit card payment process, and how they impact businesses. We will discuss all that in detail but first let’s look at the 3 main stakeholders involved in credit/debit card processing.

1. The Card Issuer- the bank that has issue the debit/credit card to the user.

2. The Card Network- the company that provides card services i.e. VISA, MasterCard.

3. The Payment Processor- the company a merchant has hired to process payments.

As a merchant, when you buy/subscribe to card payment processing services for your business, you have to incur fees for these services. The fees a merchant pays is distributed among all the players involved in the card payment processing system. On an average could range anywhere between 1.7%-3.5% per transaction. This fees is a combination of several charges of which some are fixed and some depend on other factors. Overall this fee can be referred to as the credit card processing fees. This fees is mainly a summation of:

1. Interchange Rate:

Interchange rate are non-negotiable charges that the card issuing bank levies on the merchant. A part or the whole fee is incurred by merchant regardless of the payment processor. This is generally 1.54% (per transaction) + $0.10. Interchange fee is a fixed fee which is calculated as a percentage of the total sales amount and is governed by a few factors:

- The card’s brand

- Type of card (business, debit, credit, rewards)

- Risk factor (swiped/ insertion/ typed-in/ card present or not present type)

2. Assessment/Service Fee:

Assessment fee is a small amount that the merchant pays to the credit card network company for using their services. Assessment fee when combined with the interchange rate is called the interchange fees. This fee is also a non-negotiable fee and is updated twice every year. It is about 0.11% per transaction + $0.0195 flat amount.

3. Payment Processor’s Mark-up Fee:

This is a fee levied on top of the interchange fee, it is charged by the payment processing company. This fee is negotiable and is generally a percentage of the transaction amount. It depends on a few factors like risk level of the transaction, foreign or domestic handling, network etc. Your payment processor could be a payment service provider or a merchant account provider. This is generally 2.6% + 10 cents per dip or 3.5% + 15 cents per keyed-in transaction.

A payment service provider allows online, card present and card not present which are the MOTO orders (mail order: telephone order). These providers work with a ‘flat rates’ system. On the other hand, a merchant account provider service charges at different levels.

Apart from these, there are a bunch of other credit card processing fees, take a glance here.

Recurring Flat Rates:

1. Monthly/Annual Account Fee: Charged for keeping your payment processing A/c up and running.

2. Monthly Min. Processing Fee: Minimum fee to be paid if the merchant doesn’t reach the require amount of charges each month.

3. Terminal Lease/Rent: A credit card terminal rent may be charged.

4. Withdrawal Fee: Charged when moving funds from the payment processor A/c to the merchant’s business bank A/c.

5. Statement Fee: A small fee is charged providing statements online or offline.

6. IRS Reporting fee: Fee for compiling and reporting a merchant’s transactions to the IRS (Internal Revenue Service)

7. PCI-DSS Compliance Fee: A small fee is levied for to avail Payment Card Industry- Data Security Standards.

8. Payment Gateway Provider Fee: This fee is charged for availing the ‘payment gateway’ service.

The above fees are recurring. However, there is a set of other fee that a merchant must incur, these are one time flat fees:

- Account Setup Fee: Fee paid for opening up a merchant account or payment processing account.

- Terminal Purchase Fee: Cost incurred for purchasing/buying a credit card terminal.

- Cancellation Fee: Heavy penalty can be charged upon early termination of account/contract.

There is a bundle of incidental fees that must be paid by the merchant to the payment processor company.

1. Cardholder Disputes Fee: Charged when a customer reports a dispute.

2. Chargeback Fee: Charged for every refund to the customer

3. Non-sufficient Funds Fee: For keeping less funds in business bank A/c.

4. Batch Payment Processing Fee: For a batch of credit card purchase.

As a merchant, you must be aware of these charges and make the right decision while choosing your payment service provider. Connect with us for any other assistance on credit card processing fees and rates.

More related blogs

- C-Corporation (C-Corp) Formation

- Who needs to file a BOI report?

How the Corporate Transparency Act Affects Merchant Account Approvals?

- C-Corporation (C-Corp) Formation

- Who needs to file a BOI report?

- Finance

- pci dss compliance checklist

What Is PCI DSS 4.0 Level 1 Certification and Why Is It Important?

- Finance

- pci dss compliance checklist

- Finance

- avoiding merchant account rejection based on business structure

How Your Business Structure Shapes Payment Processor Approval in 2026?

- Finance

- avoiding merchant account rejection based on business structure